Under Arizona law, by using the state’s bankruptcy exemptions, you can keep some cash and personal property that might otherwise go to the bankruptcy estate. Arizona is an “opt-out” state, meaning that instead of federal exemptions under the United States Bankruptcy Code, bankruptcy filers must use Arizona’s bankruptcy exemptions.

Article 1 of Chapter 8 of Title 33 of the Arizona Revised Statutes (ARS) Sections 33-1101 through 33-1153 contains Arizona’s bankruptcy exemptions. In this blog post, we discuss how much you can claim in cash exemptions in Arizona when you declare Chapter 7 bankruptcy or Chapter 13 bankruptcy.

To learn more about how much you may be able to claim in cash exemptions under Arizona’s bankruptcy exemptions, call the bankruptcy attorneys at Stone Rose Law. You can reach us anytime at (480) 739-2448 or contact us online.

What Are Arizona’s Exemptions That Apply to Cash?

How much cash you can keep in an Arizona bankruptcy case depends on what kind of money is involved. The following are the main categories of exempt funds.

Cash in Bank Accounts

Under ARS 33-1126(A)(9), you can exempt up to $5,600 in a single account in any one financial institution as those are defined under ARS 6-101(11) (banks, trust companies, savings and loan associations, credit unions, consumer lenders, and international banking facilities and financial institution holding companies).

If you are filing bankruptcy jointly with your spouse, you can double this exemption up to $11,200.

- In a Chapter 7 bankruptcy, any funds above this amount held in financial institutions are generally not exempt funds and are subject to trustee liquidation.

- In a Chapter 13 bankruptcy, how much of your bank accounts are non-exempt assets can have an impact on your debt repayment plan. You must pay your creditors the value of your non-exempt assets over the life of the plan, which can be from three to five years.

Wages

Under ARS 33-1131(B), the Arizona bankruptcy exemption for your wages allows you to protect up to 90% of your weekly disposable earnings. “Disposable” earnings are the funds that remain after legally required deductions, such as tax withholdings and mandatory retirement contributions.

- Exemptions apply to all kinds of income you earn, including salaries, bonuses, commissions, and pension payments.

Under ARS 33-1131(B), in some cases, instead of the 90% figure above, you can exempt an amount equal to 60 times the highest of any federal, state, or local minimum wage if this will yield a higher exemption amount.

- Wage exemptions apply in both Chapter 7 and Chapter 13, though Chapter 13 uses them differently in plan calculations.

- Similarly, under ARS 33-1131(C), only 50% of your disposable earnings are exempt from obligations to pay spousal or child support obligations.

Sources of Income That Are Fully Exempt

Under ARS 33-1126(A), the following sources of income are completely exempt in a bankruptcy filing, even if you are holding them in cash or in a bank account:

- Social Security benefits

- Veterans benefits

- Unemployment compensation

- Workers’ compensation

- Child support or spousal maintenance

- Disability, health, or accident insurance proceeds

To avoid confusion, it is best to keep these funds in a separate bank account to clearly show their exempt status. Consult with a bankruptcy attorney on how to navigate this protection.

What About Tax Refunds in Arizona Bankruptcy?

A tax refund is considered part of your bankruptcy estate, and a portion or all of it may be an unexempt asset. This means it must be turned over to pay your creditors. The Arizona Legislature updated the list of exemptions in 2025 to include child tax credits and earned income credit.

If you receive a child tax credit or earned income credit in your federal returns in addition to a state dependent care credit, these amounts are protected and deducted as funds you can keep from your total tax refund.

How much of the remaining refund the trustee can take in a Chapter 7 bankruptcy depends in part on when you file your case. A refund received early in the year represents income earned over the prior twelve months, and the trustee’s claim is typically calculated based on the portion of the year that had passed before you filed.

There are some ways to protect a tax refund before filing for bankruptcy. If you receive the tax refund prior to filing, you use the funds by spending the refund on legitimate household expenses — such as rent, utility bills, groceries, car repairs, or your attorney’s legal fees — is generally acceptable, provided you can document these expenses.

Your bankruptcy attorney can advise you on the timing of your filing to minimize the impact on your refund.

- In a Chapter 13 bankruptcy, tax refunds are treated differently because you retain your property and assets under your repayment plan. However, the value of the refund may increase the amount you must pay to your unsecured creditors over the life of the plan.

Are Retirement Accounts Exempt in Arizona Bankruptcy?

Retirement accounts are generally fully exempt in an Arizona bankruptcy case under both federal law and Arizona state exemptions. ERISA-qualified plans — including 401(k)s, 403(b)s, and pension plans — are excluded from your bankruptcy estate entirely.

Traditional and Roth IRAs are also protected under ARS 33-1126(B), which exempts money held in retirement plans. Unlike federal bankruptcy exemptions, which cap IRA protection at approximately $1.5 million, Arizona’s exemption has no stated limit on IRA protection. Arizona’s exemption also covers inherited IRAs, which are not protected under federal bankruptcy law.

There is one important limitation: amounts contributed to an IRA within 120 days before filing for bankruptcy are not exempt under Arizona law.

Because retirement accounts are protected separately from your bank account and other cash exemptions, the money in these accounts does not reduce the amount of other property you can exempt when filing for bankruptcy.

Summary of How Chapter 7 and Chapter 13 Treat Income and Cash Exemptions

| Type of Money | How Much You Can Keep |

|---|---|

|

Money in a Deposit Account |

$5,600 for single filer$11,200 for married joint filers |

| Earned Wages | Mostly exempt (90% rule)50% exempt in cases of support obligations |

| Social Security funds and veterans’ benefits | 100% exempt |

| Child support/alimony | 100% exempt |

| Unemployment compensation | 100% exempt |

| Disability, health, or accident insurance proceeds | 100% exempt |

| Tax refunds | Limited to child tax credit, earned income credit, and date of filing |

| Retirement accounts | 100% exempt (with 120-day contribution limitation) |

Does Arizona Have a Wildcard Exemption?

Federal bankruptcy law exemptions include a “wildcard exemption” under 11 U.S.C. § 522(d)(5). Arizona has no equivalent to this exemption in its state exemptions, and because you must use the state exemptions when you file bankruptcy in Arizona, no wildcard exemption is available.

What Are the Key Differences Between Chapter 7 and Chapter 13 Bankruptcy Exemptions?

The important distinction between Chapter 7 bankruptcy and Chapter 13 bankruptcy exemptions is not the dollar values of the exemptions: these do not change. Instead, the key consideration is how each chapter treats non-exempt property:

- In a Chapter 7, the trustee can liquidate non-exempt property and assets (including cash) to pay your creditors.

- In a Chapter 13, you get to keep your property and assets without liquidation, but you must pay the value of the non-exempt property and assets to your creditors through your debt repayment plan.

- This Chapter 13 difference in treatment is based on the “best interest of creditors” test, which holds that in a Chapter 13, your creditors must receive at least as much as they would in a Chapter 7.

Here is an example of how this difference works:

Let’s assume you have $8,000 in a bank savings account. You are filing for bankruptcy only for yourself (no spouse involved).

- You can exempt $5,600 from this account under ARS 33-1126(A)(9). This leaves $2,400 as non-exempt assets.

- In a Chapter 7 bankruptcy, the bankruptcy trustee can liquidate that $2,400 to pay your creditors.

- In a Chapter 13 bankruptcy, you get to keep the entire $8,000 account funds, but you must pay the $2,400 value to creditors through your payment plan.

When is Chapter 13 Bankruptcy Preferable to Protect Cash?

Many bankruptcy filers who use Chapter 7 may be surprised to learn that money they thought would be exempt turns out to be non-exempt. Even though the exemptions are the same, a Chapter 13 bankruptcy can keep non-exempt funds in your possession that would otherwise be subject to liquidation in Chapter 7.

Chapter 13 can be better than Chapter 7 bankruptcy to protect money in the following situations:

- You have large balances of money in financial institutions.

- You have received a recent tax refund.

- You have a significant amount of cash on hand through your business.

- You have received proceeds from a home sale.

- You have irregular sources of income.

What Happens to Cash You Spend Before Filing for Bankruptcy?

If you have non-exempt cash that exceeds what you can protect through Arizona’s bankruptcy exemptions, spending that money on reasonable and necessary expenses before filing is generally permitted. Legitimate uses of cash before filing for bankruptcy include paying rent or mortgage payments, keeping up with utility bills, buying groceries and household supplies, making car repairs, and covering medical expenses.

However, the bankruptcy trustee and the bankruptcy court will review your spending cash and other financial activity in the months before you filed. Certain payments can cause problems:

- Repaying a debt to a family member or friend within one year of filing may be treated as a preferential transfer, which the trustee can reverse.

- Making luxury purchases or taking cash advances shortly before filing for bankruptcy can be treated as presumptively fraudulent, and the resulting debts may not be eligible for a bankruptcy discharge.

- Large cash withdrawals without documentation of how the money was spent will raise questions from the trustee.

It is advisable to keep detailed records of your expenditures and use your checking account or debit card rather than cash to create a clear paper trail. A bankruptcy attorney can help you plan your spending before filing to avoid any appearance of bankruptcy fraud.

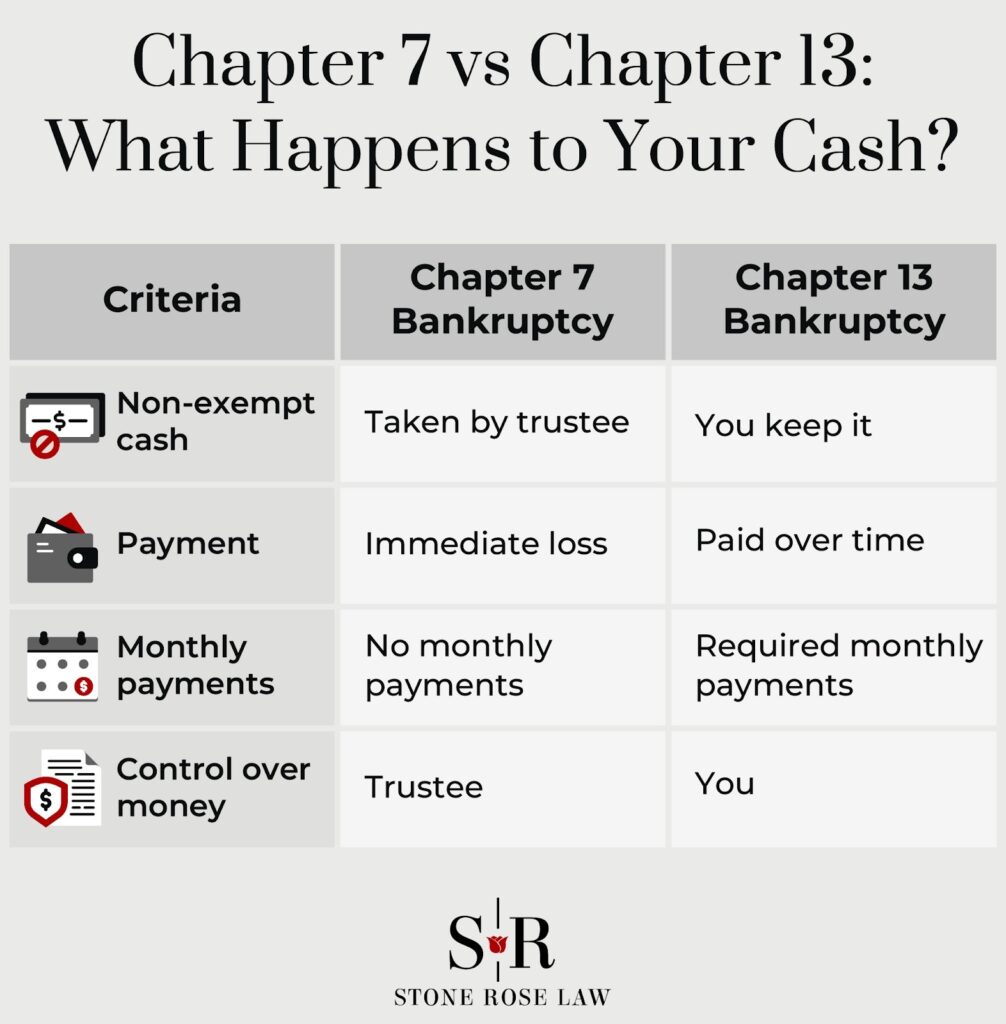

Summary of How Chapters 7 and 13 Apply to Money Exemptions

| Issue | Chapter 7 | Chapter 13 |

|---|---|---|

|

Can you keep non‑exempt cash? |

Usually no | Yes |

| How is non‑exempt cash allocated? | Immediate loss | Paid over time |

| Monthly payments | None | Required |

| Who controls money | Trustee controls | You control |

Do You Have Questions About How to Keep Cash in Bankruptcy?

Whether to use the Chapter 7 bankruptcy or the Chapter 13 bankruptcy process is a choice that must account for several factors; protecting assets like income and cash through Arizona’s statutory exemptions is one of them. An experienced bankruptcy lawyer can advise you on which form of bankruptcy is best for you, and can also give you legal guidance on debt relief alternatives to bankruptcy.

At Stone Rose Law, our Phoenix bankruptcy attorneys have decades of experience representing clients in bankruptcy cases. In a free consultation, we can review your unique debt situation, including your assets and how to protect them from liquidation. You can reach us at any time, day or night, by calling our law offices at (480) 739-2448 or by using our online contact form to speak with one of our bankruptcy attorneys about how to protect your personal property in a bankruptcy case and to file a bankruptcy petition if this is the right option for you.

The post How Much Cash Can I Keep in Bankruptcy? appeared first on Stone Rose Law.