Chapter 7 bankruptcy offers many advantages as a means of debt relief through debt discharge. But first, you have to qualify to use it, and that means passing the means test.

If you want to know if you qualify for Chapter 7 bankruptcy, please call Stone Rose Law at (480) 739-2448 to get a free consultation with a Washington bankruptcy lawyer.

What is the Means Test for Chapter 7 Bankruptcy?

The means test is a way to make sure that Chapter 7 bankruptcy is reserved for people who really cannot afford to pay their debts. The means test has been part of the Chapter 7 bankruptcy calculation since its introduction in the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005. The means test prevents people who have the income to pay their debts from abusing Chapter 7 to take advantage of creditors.

The Chapter 7 means test applies to individuals who have primarily consumer debts, not business debts.

How Does the Chapter 7 Means Test Work?

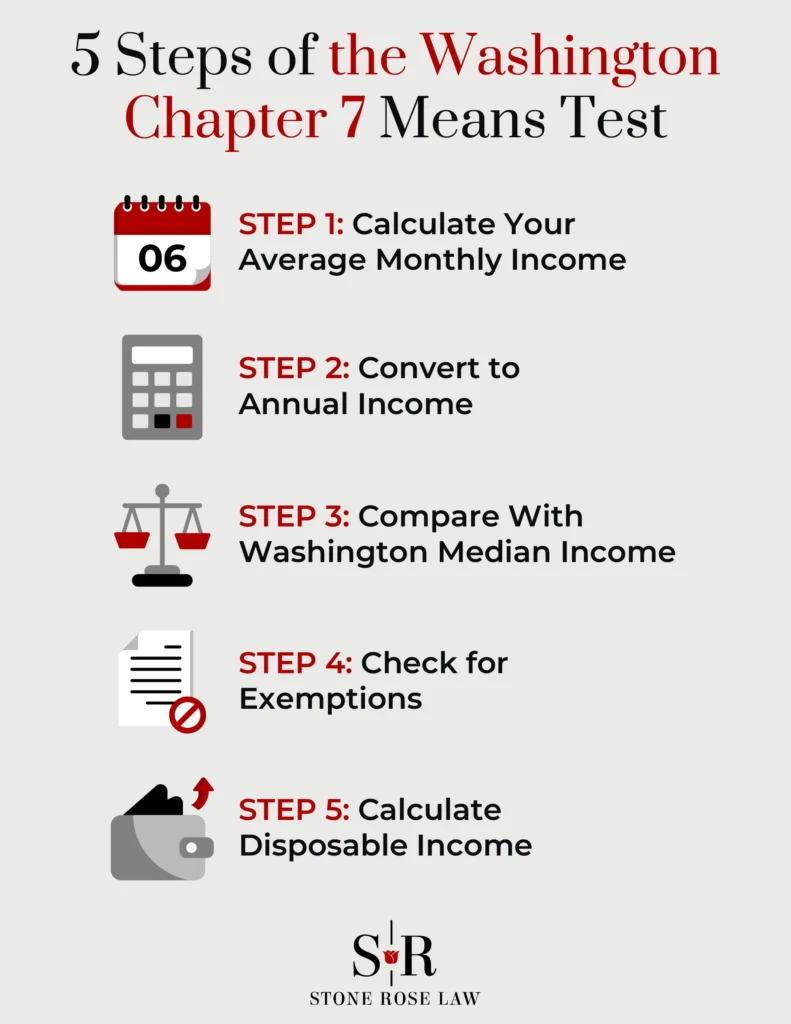

The Chapter 7 bankruptcy means test in Washington is a multi-step process.

Step One: Before the Means Test, Determine Your Average Monthly Household Income

In the first part of the means test, you compare your household’s current monthly gross income (before taxes and deductions) to the median gross income limit for a household of the same size in Washington state.

To begin, add up your gross income for the last six months, then divide by 6 to get your average monthly income, and then multiply that number by 12 to get your annualized gross income.

What Counts as Income?

Income for the means test is determined under Bankruptcy Code §101(10A) and Official Form 122A-1. Some income sources, like certain disability and federal benefits, may be excluded or partially excluded even if counted on Schedule I.

What is Not Considered Income?

Not all income is included in the means test. Examples of income sources you may exclude are:

- Social Security retirement income

- Social Security Disability Insurance

- Social Security Supplemental Security Income

- Disability payments you receive through the U.S. Department of Veterans Affairs (VA)

- Money you receive as damages for personal injuries

- Payment you receive as a victim of a war crime, terrorist act, or crime against humanity

- Some court-ordered victim payments

- Income from repayment of a debt and loan proceeds

- Tax refunds

What Is Your Household Size?

For bankruptcy purposes, your household includes individuals financially connected within a single dwelling. This means your immediate family, dependents, and anyone who relies on or contributes to the household’s resources.Usually, your household size is easy to determine. Sometimes it may be more complicated to determine, such as when children reside with you part-time or you have adult children living in the residence. A Washington bankruptcy lawyer can help you determine if these family members are part of the household.

Step Two: Calculate Your Annual Household Income

Take your monthly average gross income above and multiply it by 12. This is your median household annual gross income.

Step Three: Compare Your Annual Household Median Income to the Current Washington Median Income

The means test relies on data provided by the U.S. Census Bureau. This data is updated approximately every six months. As of November 1, 2025, Washington state’s median income levels are:

|

Household Size |

Median Annual Income Limit |

| 1 | $86,314 |

| 2 | $104,354 |

| 3 | $128,360 |

| 4 | $152,553 |

For each additional household member beyond the first four, add $11,100. So, for example, for a household with five members, the annual Washington median income for the period beginning November 1, 2025, is $163,653.

If your median income is below the state median, you are not subject to a presumption of abuse and generally do not complete Official Form 122A-2. However, you do complete Official Form 122A-1 and still report income.

Step Four: Are You Exempt From the Means Test?

Some people do not need to take the Chapter 7 bankruptcy means test:

- If your debts are primarily business debts or other non-consumer debts (more than 50% of your total debt). Examples include business car loan payments or amounts you owe to vendors.

- If you are a disabled veteran and incurred most of your debt during active duty or while serving in homeland defense activities. The disabled veteran exemption applies if at least 50% of your debts were incurred while on active duty or homeland defense activity, and you have a 30% or greater service-connected disability rating or were discharged due to disability.

- If you were a member of a reserve component of the U.S. Armed Forces and were called to active duty after September 11, 2001, and served for at least 90 days on active duty, then you are exempt for up to 540 days after your active duty service ends.

Step Five: If Your Household Annual Median Income Exceeds the Washington Median Income

If your annual household income exceeds the Washington median income level, you may still qualify for Chapter 7 bankruptcy if your monthly expenses are high enough to reduce your disposable income to less than the threshold amount.

You will need to complete three forms as part of the means test:

- Official Form 122A-1Supp (Statement of Exemption from Presumption of Abuse)

- Official Form 122A-1 (Statement of Your Current Monthly Income) and

- Official Form 122A-2 (means test calculation)

The means test can be complex. It is necessary to determine your disposable income using a formula, deduct allowed expenses, and then multiply by 60 months. You must provide information based on national, Washington, and local averages and standards based on Census Bureau and the Internal Revenue Service data, including:

- Your Washington median household income (see above)

- Your Food, clothing, and other expenses

- Your out-of-pocket healthcare expenses

- Your local housing and utilities expenses

- Your local transportation expenses

We recommend having an experienced Washington bankruptcy attorney assist you with your means test forms to ensure they are completed accurately.

Once you have gathered all the required information, you subtract all your allowed expenses for Washington from your income to determine how much income you would have available to pay your unsecured creditors in a Chapter 13 debt repayment plan. Under 11 U.S.C. §707(b)(2), if your allowed disposable income multiplied by 60 months exceeds the applicable threshold in the statute, then a presumption of abuse arises.

Note that even if you pass the means test, sometimes the bankruptcy trustee may seek to dismiss your Chapter petition based on “totality of the circumstances” considerations.

What Happens If You Fail the Bankruptcy Means Test?

If you do not pass the Chapter 7 bankruptcy means test, you may have other bankruptcy options like a Chapter 13 bankruptcy payment plan or other debt relief options like credit counseling, debt settlement, a debt management plan, or debt payoff planning.

Talk to a Stone Rose Law Bankruptcy Attorney About Chapter 7 Bankruptcy

If you qualify, Chapter 7 bankruptcy can eliminate many of your unsecured debts and some of your secured debts through discharge. As long as you are below the income limit for the Chapter 7 means test, then filing for Chapter 7 can be straightforward. But if you make enough income to have to take the means test, then its plethora of forms and income and expense calculations can be hard to navigate.

At Stone Rose Law, our Washington bankruptcy attorneys have the knowledge and experience to go over your financial affairs to see if Chapter 7 is your best option, and to help you file in federal bankruptcy court if it is. Call us at (480) 739-2448 or use our online contact form to schedule a free initial consultation with one of our experienced bankruptcy lawyers.

The post The Washington Bankruptcy Means Test: Chapter 7 appeared first on Stone Rose Law.